WOMEN’S FASHION(*): COUNTRY-BY-COUNTRY ANALYSIS OF FOREIGN TRADE

(JANUARY-OCTOBER 2013)

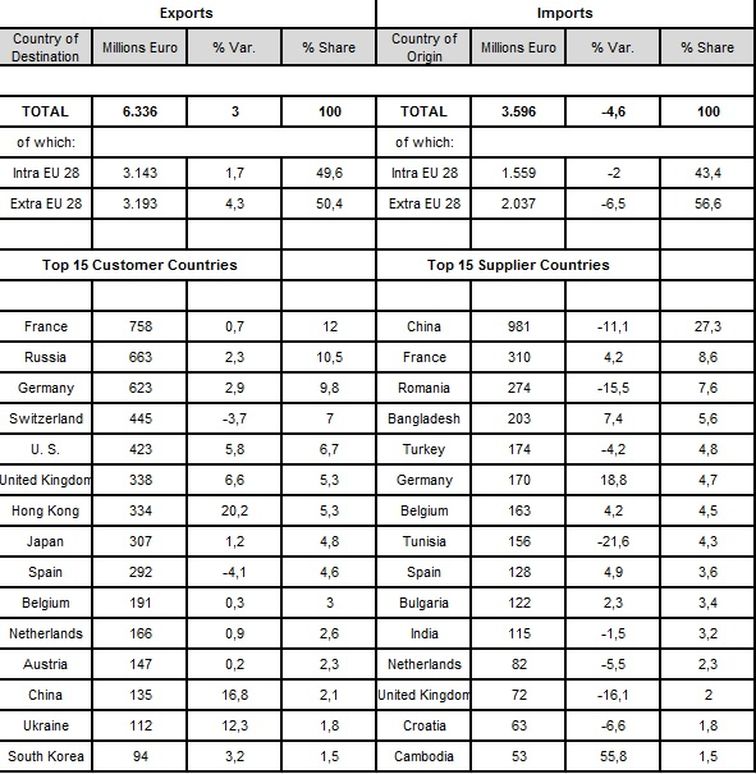

Source: ISTAT data processed by SMI

(*) – this aggregate includes Junior products

As concerns the extra-EU area, purchases by Russia (Italy’s second customer market) were up to 663 million euro thanks to a +2.3% growth rate. Exports to the U.S. market also showed a satisfactory variation (+5.8%), for a total of 423 million euro. Another positive performer was Japan, with a 1.2% growth rate.

But the most interesting growth rates were those for sales to Hong Kong and China. Hong Kong, after its 2012 “breather,” jumped by +20.2%; similarly, China was up again, with a +16.8% that brought this country’s imports of Italian women’s fashion to 135 million euro.

Turning to analysis of Italy’s supplier markets, there was another drop in goods incoming from China (-11.1%), which brought the country’s incidence on total sector imports down from the 29.3% of January-October 2012 to 27.3% in the corresponding period of 2013. Despite everything, however, China has a firm hold on its rating as Italy’s top supplier, with a total sales of close to 1000 million euro.

France, with a positive +4.2% upturn, took second place after passing Romania, which dropped back by -15.5%. Incoming flows from Bangladesh were still rising, with, specifically, a +7.4% increase (following on a double-digit increase in 2012) for 203 million euro. Also rising were the tides of imports from Spain (+4.9%) and from Bulgaria (+2.3%).

Disaggregating the overall datum by product line foreign sales of the monitored goods was characterized, in general, by positive dynamics from January through October 2013. In the exports by the preponderant sub-sector (that is, women’s fabric outerwear) increased by +2.4%, knitwear exports were up +3.1%, and exports of women’s shirts accelerated by +3.8%. The best-performer segment was leather apparel, with an increase of +9.6%.

On the other side of the scale (that is, in the case of imports of items of women’s apparel from abroad), there was a decrease not only in fabric outerwear (-5.7%), but in knitwear (-4.3%) and leather clothing (-3.7%) as well. Imports of women’s shirts were instead heading upstream, with an increase on the order of +1.7% (but with quantities still falling).

{kind=link}